CCP Greyscale Comments on Tech 2 BPOs

Posted: 2014-04-28 Filed under: industry, market, ships | Tags: bpo, broadsword, claw, claymore, huginn, mastadon, muninn, revelations, tech 2 3 CommentsWe got hit with two industry Devblogs today as it looks like CCP is going to try to publish all six industry related blogs before Fanfest. On page 9 for the comments for the Researching, the Future post, CCP Greyscale made a comment on how much Tech 2 BPOs dominate the market.

Right, Mastadon, Claymore, Claw etc are BPO-dominated, so in practice all this means is more throughput and (presumably) cheaper prices.

Huginn and Muninn are in the area of concern, where we might end up warping the market a little.

Broadsword’s not a concern because it was released in Trinity (winter 2007) and to the best of my knowledge we stopped putting new ship BPOs into the lottery in Revelations 1 (winter 2006). If that market’s uncompetitive, it’s because of your fellow inventors, not BPO owners 🙂

This adds a little more information from what we got out of CCP Diagoras before he left CCP that I covered in my Percentage of Items from Invention vs Tech 2 BPOs post.

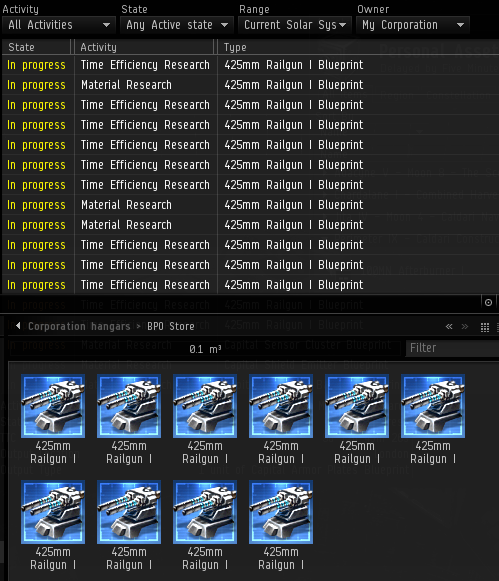

Saying Goodbye to Railgun Compression

Posted: 2014-04-11 Filed under: eveonline, industry, ships | Tags: 425mm railgun i 4 CommentsIt is with a heavy heart that we must say goodbye to 425mm Railgun I mineral compression. The broken mechanic of mineral compression is finally going away as outlined in CCP Ytterbium’s Reprocess all the things! post.

This change affects our nullsec/lowsec capital production line to the point where we have to change our entire material acquisition, hauling, and building operations around.

Raath and I have spent a few hours talking about how to rework the production lines, but we can’t come up with a acceptable solution at the moment. We’re going to be halting our production lines and are going to take a small break. Hopefully some more changes come out around Fanfest time that will inspire us.

I am in no way against this change. It is a very positive one and has been needed for years so I welcome the new challenges we’re going to have with getting minerals around the Universe.

Carrier Runs 1-228

Posted: 2014-04-09 Filed under: industry, ships | Tags: archon, chimera, nidhoggur, thanatos 4 CommentsOverview

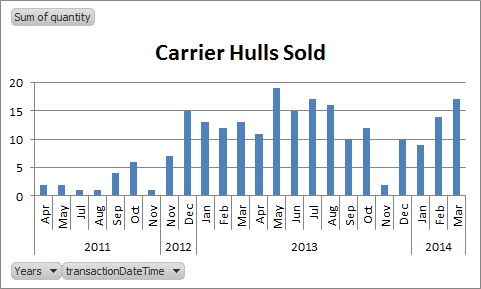

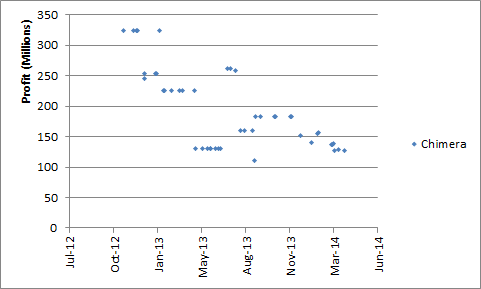

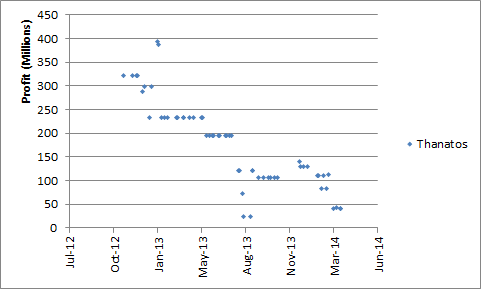

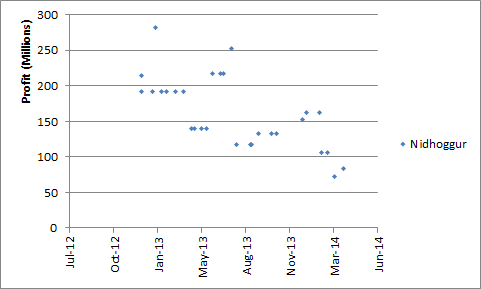

Carrier building operations have been running for 1,087 days and has generated 53.7 B in profit averaging 234.6 M/hull with a sale every 4.7 days.

There was a slight dip in production due to relocating our Capital building operations and my move across the country around November of 2013. Since then we’ve been steadily optimizing our operations and final March production counts came in at 17 hulls, almost matching our maximum of 19 in May of 2013.

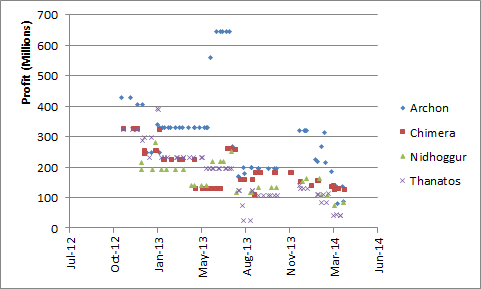

Profit Charts

The profit trends on all hulls show a downward trend.

Chimera and Archon hulls are still holding strong while Thanatos and Nidhoggur hulls are not worth producing.

Future

We are not the only capital builder noticing shrinking profits as noted also by EVE-Fail. The upcoming mineral compression changes have us rethinking our logistical operation and possibly putting our capital building operations on hold.

Expanding Dreadnought Production

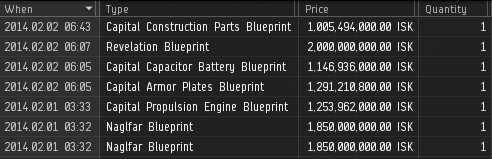

Posted: 2014-02-10 Filed under: industry, ships | Tags: naglfar, revelation Leave a commentGiven the growing popularity of Naglfar and Revelation hulls, I made a decision to expand the Dreadnought production line by adding more blueprints. The total for 2x Naglfar, 1x Revelation, and additional component BPOs to balance the ratio of blueprints came out to 10.397 B.

Four component BPOs were needed to balance out the ratios of our current Carrier and Dreadnought line. Calculations for optional ratios can be found from this post when we started building Carriers.

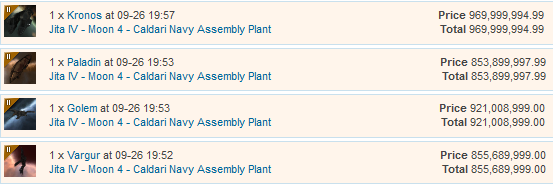

Marauder Speculation

Posted: 2014-01-22 Filed under: ships | Tags: golem, kronos, marauder, paladin, rubicon, vargur Leave a commentI was late to the party and purchased a set of racial Marauders after the Rubicon expansion. On a lazy afternoon I found them sitting in a hangar and went to check the current prices and noticed that they did in fact go up quite a bit.

I sold them off and came back with a profit of +713M. Not bad for sitting around collecting dust while I was moving across the country.